| Old Articles | | Friday, February 08 | | · | |

| Wednesday, February 06 | | · | |

| Tuesday, February 05 | | · | Savage Capitalism or Socialism: A Conversation with Luis Britto Garcia |

| Sunday, February 03 | | · | Canada vs. Venezuela: The Background Gets Even Murkier |

| Thursday, January 31 | | · | |

| Monday, January 28 | | · | The History - and Hypocrisy - of US Meddling in Venezuela |

| · | Canada Is Complicit in Venezuela's US-Backed Coup D'état |

| Wednesday, September 26 | | · | Why Israel Demolishes: Khan Al-Ahmar as Representation of Greater Genocide |

| Friday, September 21 | | · | US Disregard for International Law Is a Menace to Latin America |

| Saturday, August 25 | | · | How Long is the Shelf-Life of Damnable Racist Capitalist Lies? |

| Thursday, August 09 | | · | Martial Law By Other Means: Corporate Strangulation of Dissent |

| Wednesday, August 08 | | · | North Korea and The Washington Trap |

| · | Venezuela Assassination Attempt: Maduro Survives but Journalism Doesn't |

| Sunday, May 20 | | · | The British Royal Wedding, Feelgoodism and the Colonial Jumbie |

| Friday, May 04 | | · | |

| Monday, April 09 | | · | The Bayer-Monsanto Merger Is Bad News for the Planet |

| Tuesday, March 20 | | · | Finally, Some Good News |

| Thursday, March 15 | | · | Zimbabwe Open for Business, Code for International Finance Capitalism |

| Friday, January 12 | | · | Shadow Armies: The Unseen, But Real US War In Africa |

| Wednesday, December 13 | | · | The U.S. is Not a Democracy, It Never Was |

Older Articles

| |

| |

World Focus: Money Manager Capitalism: Oil Imperialism and Monetary Policy

Posted on Sunday, March 22 @ 16:49:53 UTC

Topic: US Foreign Policy

|

By ROB URIE By ROB URIE

March 22, 2015 - counterpunch.org

In important ways the world is an eternal mystery and in significant ways it isn’t. On the side of mystery are pre and post cognitive understanding, being of and in the world and all of the irreducible relations these entail. On the other side is narrative form, the way that the world is understandable in a communicable sense. A central strategy in the politics of domination is to convince us that the latter is the prior— that public policies are existential mysteries that need to be left to official interpreters lest they be misinterpreted. This has been alternatively explained as those who control the present control the past, with the past being history as shared narrative.

U.S. foreign policy in its official dimension is often an unfathomable mystery, a series of unrelated events that policy officials manage on a case by case basis. Within the taxonomy of modern academia this is the realm of political science. In another dimension lies pure economics; deduced theories about how ‘the world’ works where the economists’ hammer sees everywhere and always isolated and detached nails. And in yet one other dimension is the intersection of economics and politics, political economy of past decades. If economic interests can be found to substantially drive political actions, e.g. U.S. foreign policy, political scientists join economists in controlling the present through improbable parsing of the past.

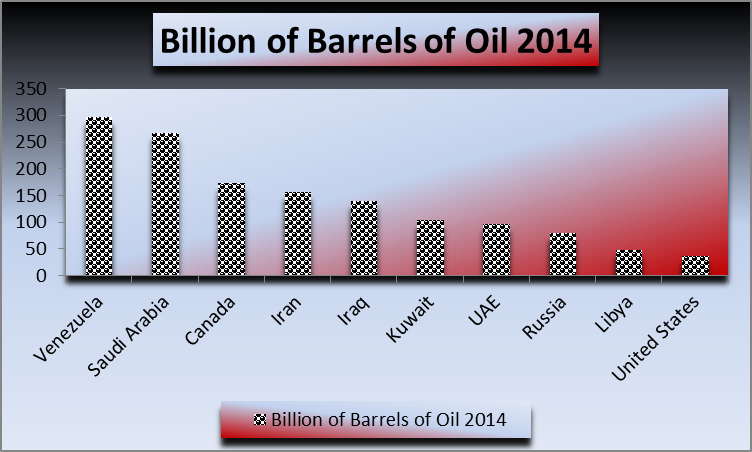

Graph (1) above: with U.S. President Barack Obama declaring Venezuela a “threat to national security” a political patina is applied to the economic interests of U.S. based multi-national oil companies. Venezuela has the largest proved reserves of oil in the world and the (President Nicolas) Maduro government wants to use it to provide for the people of Venezuela. Al Qaeda attacks on 9/11 were in large measure a reaction to U.S. military bases in Saudi Arabia. Canada’s oil is inefficient (costly) to extract. The Iran-Iraq War found the U.S. supplying both sides with arms while using Iraq to try to force Iran back into the U.S. sphere of influence. Current Obama administration reconciliation with Iran has Iranian and Iraqi oil flowing through U.S. pipelines to Europe. The ‘savage’ ISIS (Islamic State) could spend the next century in Iraq and only a fraction of the carnage caused by the U.S. invasion would result. The Kuwaiti oil industry was started by what are today BP and Chevron. The first Gulf War resolved an oil dispute between Iraq and Kuwait in Kuwait’s favor. The U.S. facilitated coup in Ukraine is a conflict with Russia over who supplies Europe with oil and gas. Libya was substantially destroyed by the U.S. and France to control Libyan oil. Source: EIA.

The theoretical distance between ‘the political’ and ‘the economic’ in Western discourse leaves space in the middle that falls to Marxian exposition. Western economic interests — multi-national corporations and bankers living on the public dime; have ‘caused’ the overwhelming preponderance of U.S. foreign policy over the last century. Graph (1) above relates proved oil reserves to U.S. military encumbrances past and present. The current cartoon boogeymen of ISIS, Russia and the government of Venezuela depend upon wholly contrived ‘histories’ for their power to convince an apparently unquestioning public that any plausible threat exists. With actual U.S. history and the facts in hand, plausible motives for demonization by the U.S. are control of oil, control of oil and control of oil, respectively.

History

In significant ways the 1970s represent the key to modern history. Despite Cold War bluster that the unipolar world began with the ‘fall’ of the Soviet Uni0n in the early 1990s, the period of U.S. economic and political hegemony lasted from approximately 1945 to the early 1970s. With the only substantial industrial infrastructure left intact after WWII, the U.S. set about rebuilding ‘the West’ with it as the monetary, economic and military center within the frame of ‘benevolent hegemon.’ The Bretton Woods system implemented in 1945 was intended to foster U.S. dollar hegemony centered on a ‘managed’ gold standard. The Marshall Plan rebuilt the industrial bases of Europe to play a supporting role to American industry. And the U.S. military bases created at the time still litter the world.

By the early 1970s the industrial bases of Europe and Japan had fully recovered and the limits on monetary expansion under Bretton Woods pushed up against the U.S. role as military hegemon and the need to placate domestic tensions with increased public spending. Overseas production of oil and gas ended U.S. monopoly control over global oil prices. The Vietnam War that ended in 1975 had been widely known to be a lost cause by policy insiders as early as the mid-1960s. And in 1971 U.S. President Richard Nixon unilaterally abandoned the gold standard of Bretton Woods effectively ending the accord and with it crucial aspects of U.S. dollar hegemony, particularly with respect to global oil and gas production.

The first ‘Arab Oil Embargo’ of 1973 was placed in a geo-political frame that had alternative explanation in economic interests. The Texas Railroad Commission that had controlled global oil prices from the 1930s through the early 1970s didn’t voluntarily end its control over prices. By 1970 U.S. oil producers were producing at maximum capacity requiring large scale oil imports to support domestic industrial production. Overseas production filled the difference in global energy needs. Under the terms of Bretton Woods oil priced in U.S. dollars linked to the price of gold tied the price of oil to the price of gold. U.S. abandonment of the Bretton Woods Accord broke this link at a time when U.S. dollars were depreciating relative to the newly floating ‘official’ price of gold. From the non-USD (U.S. dollar) perspective the dollar price of oil was falling. This was against an extended period when the Texas Railroad Commission had let the real (inflation adjusted) price of oil decline.

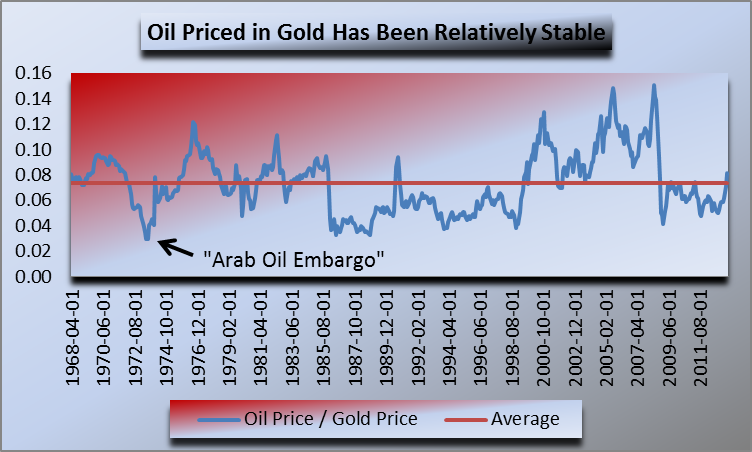

Graph (2): when the U.S. unilaterally abandoned the Bretton Woods accord the price of gold began to rise relative to the price of oil. The end of the USD link to the price of gold led to de facto depreciation of the value of assets denominated in USD. Gold serves as a standalone currency in the hawala money system used across Asia and the Middle East— breaking the link of the USD to gold had detrimental consequences amongst overseas oil producers. And despite fluctuations that persisted for extended periods, the price of oil in terms of gold has remained relatively stable across the last five decades. Source: St. Louis Fed.

The Tehran Agreement of 1971 temporarily linked the price of oil to a basket of currencies that continued to trade relative to the price of gold. This temporary fix broke when the EEC and Japan formally abandoned Bretton Woods in 1973. Gold plays a role as currency through the hawala money system across Asia and the Middle East. Under the Bretton Woods system U.S. dollar hegemony had supported the interests of the U.S. When, for a combination of political and economic reasons, it was no longer in the U.S. leadership’s interests to continue the system the Nixon administration unilaterally abandoned it. In the context of rapid USD depreciation, this amounted to the U.S. unilaterally deciding to pay less for overseas oil. Another way to say this is that USD inflation was de facto depreciation of the value of overseas oil in USD terms.

In recognition of changed U.S. circumstance U.S. President Jimmy Carter launched the ‘Carter Doctrine’ in 1980 expanding U.S. military reach across the Middle East to maintain control of global oil supplies. This followed the Iranian Revolution of 1979 and a consequence was the U.S. pivot toward Israel. The ‘strong dollar’ policy of the (Ronald) Reagan administration can be seen in part as an effort to retain USD hegemony. Carter appointee to the Federal Reserve Paul Volcker engineered what was at the time the worst recession in modern history to ‘break the back of inflation’ that in fact served to support the value of petrodollars. This recovery of USD hegemony today is under broad attack with non-USD currency agreements being negotiated between Russia and China, across Asia and more recently with Germany, France, UK, Italy and Australia joining the Asian Infrastructure Investment Bank.

The points of relevance are the relation of the breakdown of the Bretton Woods monetary uni0n to international oil economics that have been framed in terms of geopolitics. This isn’t to deny the ‘fact’ of geopolitics, but rather to provide economic motives to otherwise ‘emotive’ political rationales (e.g. “they hate us for our freedoms”). In theoretical terms the post Bretton Woods ‘fiat’ role of the USD makes explicit the social-historical role of money. Outside of this history the use of gold as money is arbitrary. But within it gold retains an embedded role as money in some cultures. Given the political-economic role of gold standards in precluding competitive currency devaluations, at least in theory, it is safe to assume that Richard Nixon’s decision to unilaterally abandon Bretton Woods wasn’t lightly undertaken (voluntary). Neither was the decision of the Texas Railroad Commission to abandon its role as cartel global oil price setter.

Geo-Political Misdirection

Between U.S. wars in Korea, Vietnam, Cambodia, Laos, Iraq, Nicaragua, El Salvador, Honduras, Somalia, Yemen, etc. ad infinitum the body count of murdered innocents exceeds that of the Nazis in WWII. The atrocities committed in each of these wars are among the more hideous and wholly unnecessary in human history. Under no conceivable configuration of circumstance could any of these nations or their peoples have posed a plausible threat to the citizens of the U.S. The U.S. strategy in Vietnam and that in Nicaragua articulated by the CIA was ‘war of attrition,’ destroying enough schools, roads, hospitals and human lives that people would rebel against their governments. U.S. use of illegal white phosphorous to slaughter the captive population of Fallujah burned an entire city of human beings alive.

Once these truths of modern American history are granted pious nonsense about protecting freedom and promoting democracy abroad can be seen for what it is— cynical misdirection. The greatest gift to peace and prosperity the world could see is the end of the U.S. as military, political and economic hegemon. This written, with no thanks due to internal opposition, the unwind seems to be several decades underway. The initial pivot came in the early-mid 1970s when OPEC, including Venezuela, first called out USD hegemony with an oil suppliers strike. Aiding the effort were U.S. based multinational oil companies that held tankers full of oil offshore to raise the price. But we’re all in this economy together, right?

As the official dissemblers in the press have it geo-politics, mainly the threat of ‘terrorism,’ is the main driver of U.S. foreign policy. Given U.S. history and the murderous regimes the U.S. regularly installs and / or supports, the more plausible explanation is state support for economic interests. As Graph (1) above illustrates, U.S. foreign interests can be more plausibly explained as:

Venezuela: oil

ISIS in Iraq and Syria: oil

‘Russian aggression in Ukraine’: oil

The Iranian ‘nuclear program’: oil

Libya: oil.

The central challenge for official explanations of U.S. foreign policy is that the U.S. regularly supports the actions it claims to oppose. Venezuela has freer and fairer elections than the U.S. With the Obama administration’s punishment of domestic whistleblowers, effectively destroying their lives, the complaint that Nicolas Maduro is putting U.S. spies and coup-fostering plutocrats in prison is laughable. Those who consider ISIS savage should revisit U.S. actions in the Vietnam War, the Reagan era wars in Central America (link above) and (George W) Bush’s war in Iraq. NATO (the U.S.) has unilaterally broken NATO expansion agreements made with Russia since the fall of the Berlin Wall. The contention that Iran has a nuclear weapons program has been repeatedly disputed by the entirety of the U.S. intelligence community. Libya today is a prime example of what U.S. ‘democracy’ looks like, a failed state.

Domestically, nominal citizens have been made so much fodder for this same foreign policy turned inward. When Al Qaeda, created and funded by the CIA, brought down the twin towers an ‘official’ wish list of levers of internal repression was unleashed. The right-wing claim that this is the result of government ‘overreach’ overlooks the public-private partnerships behind the increasingly privatized and militarized surveillance-police state and that many of the ‘domestic terrorism’ proscriptions are to limit harm to economic interests. Environmental and animal rights activists are seen as the primary domestic ‘terrorist’ threats. And the Obama administration’s economic policies viewed through the lens of actual outcomes had restoration of the power structure that existed before the crisis of 2008 as their singular goal.

Monetary Policy

The unilateral withdrawal by the U.S. from the USD – gold link of Bretton Woods effectively ended the formal monetary system while leaving in place its central institutions, the IMF and World Bank. The framework for fixed-exchange rate workouts in a world with pseudo-restricted public money flows and largely unrestricted private money flows can be seen being applied across peripheral Europe in the present. In both the U.S. and continental Europe a contrived budget ‘constraint’ is put forward as a limitation on national accounts while Central Bank monetary policies support an unrestricted and predatory private money system, a/k/a Wall Street. Even (especially) Western liberals are pushing the fallacy of budget constraints that Richard Nixon rendered irrelevant in 1971. The European currency uni0n created a pseudo-gold standard through fixed currency values within the uni0n. But as the Syriza Party in Greece is fond of pointing out, a Euro in Greece isn’t worth as much as it is in Germany.

The role of the U.S. Federal Reserve in 2007 – 2008 was as ‘the world’s’ Central Bank, doling out USD swaps while insiders were loading up the life-rafts with insider deals on the stocks of soon to be bailed out banks. The attendant crimes, special privileges and implausibly serendipitous coincidences have been copiously documented elsewhere and needn’t be repeated here. But they do pose a challenge for economists who claim that the Federal Reserve is acting in the public interest. At any rate, the ghost of Bretton Woods remains present today in faux fiscal constraints. As the Russian delegation had it in 1945, Western Central Banks taking clues from the U.S. Federal Reserve are acting as adjuncts of Wall Street. And a peculiar delusion known as the ‘loanable funds’ model finds Central Banks placing private debts on public balance sheets under the ruse that bank credit and fiscal expenditures all draw from the same pool of already existing money.

A key to the loanable funds delusion is the ‘zero’ lower bound, the ‘natural’ rate of interest that produces full employment but that in extraordinary circumstances can’t be achieved because it is negative. The causal mechanics of how interest rates relate to the level of employment require a singular tautology: savings = investment. Loanable funds are savings converted into investment loans made by banks. The problem with this formulation is that banks don’t loan out savings. Bank loans create deposits (savings). As Keynes likely had it, this leads to as many ‘natural’ rates as there are bank loans outstanding. Deference to nature, as in a ‘natural’ rate, is straightforwardly secular theology, an effort to hide one’s argument behind an ‘external’ totalizing intelligence. Central Banks can target an ‘official’ interest rate, but it represents the cost of money to banks— it bears dubious relation to the cost of ‘private’ credit.

The zero lower bound refers to the ‘official’ price of money, the ‘official’ interest rate. Bank money, which represents the overwhelming preponderance of money in (digital) existence, cares little about the official rate. In theory the ‘natural’ rate on bank money (loans) is a risk and liquidity spread, or addition, placed atop the official rate. But banker preference is to lend against existing collateral, be it real property or financial assets, rather than a good business plan. Additionally, there is an insider / outsider differential— in 2006 and again today banks would lend a leveraged bond portfolio money for 1% while lending poor people money to buy a house or a car (a/k/a collateral) money for 10%. The risk of loss on a 10X levered bond portfolio is much, much greater than on a house or car. With the ‘zero lower bound’ theory economists assume economic incentives that are largely irrelevant to the private money system.

By analogy, in capitalist economic theory corporate executives, ‘agents,’ act in the best interests of the ‘stakeholders’ of ‘their’ corporations. In recent decades stakeholders have been reduced to shareholders. How can executives take care of themselves by taking care of shareholders? They do so by granting themselves large ownership interests (link above) in ‘their’ corporations. The analogy ties to the ‘zero lower bound’ through the self-dealing capacity of Wall Street banks to underprice the ‘natural’ rate that applies to financial speculation. Wall Street bankers, including large European banks, knew that the Greek people’s capacity to repay public debt was lower than Germany’s. But because bank regulations assigned equivalent values in bank capital requirements, the ‘logical’ trade was out of German Bunds and into Greek public debt. Large European banks, a/k/a Wall Street, are directly responsible for the ongoing misery across the European periphery.

Money Manager Capitalism

While modern finance has developed incrementally from mathematical theories of randomness to efficient markets to behavioral finance, viewed from the present without the theoretical baggage one could fairly assume that a global idiot bomb went off. The Wall Street ‘sell side’ creates products of dubious quality and the ‘buy side’ rewards those who buy the worst crap available when markets are rising and who lose incrementally less than the next person when they tank. These are never the same people. This is to write that a well-trained chimpanzee could outsmart the smartest folks on Wall Street if it knew when markets would rise or fall. This isn’t a gratuitous slam— the outcome is a function of the Federal Reserve’s increasing instantiation and commodification of finance over the last forty years.

To broaden the idea, when (Hyman) Minsky wrote of money manager capitalism he was referring to both investment banking and asset management. Bank money is the substance, the ‘fluid,’ needed to transform General Electric from an industrial company into a hedge fund, the transformation being an investment banking function. Asset managers ‘motivate’ the transformation process by coercing company executives to fire actual workers to ‘refocus’ the business on leveraged subprime car loan and credit card receivables. The Federal Reserve’s roles are to provide copious cheap money to the banks to facilitate the process and to guarantee that no matter how badly company executives and financiers screw things up they will walk away (or worse yet, stick around) very rich people.

The charge that Federal Reserve polices cause mal-investment gets to the heart of the loanable funds model, and with it the ‘zero lower bound’ delusion. In practical terms, with corporate profits taking a near record share of national income (GDP), the question of why Western corporations are buying back ‘their’ shares rather than investing in productive capacity comes to the fore? In capitalist economic theory profits tie to the return on productive activity. If they don’t, and share buybacks suggest they don’t, then profits don’t play the role in capital allocation that justifies their existence in capitalist economics. Put differently, why should today’s executives receive outsized paychecks for decisions made twenty years ago and that are paying off today because the Federal Reserve has flooded the world with money?

To make this explicit should actual economists venture hither: the zero lower bound argument is that in present circumstance the official interest rate over which the Federal Reserve has control should be negative— persons and companies should be paid to borrow money. To the extent that private credit— bank money, is underpricing risk, persons and corporations are being paid to borrow money. Why would banks knowingly underprice risk? To provide the generalized answer preferred by economists I defer to Philip Pilkington. To paraphrase: the ‘natural rate’ is a static concept, it is premised on inferring current circumstance eternally forward. Corporate debt has an average life of ten years while the natural rate is only relevant to circumstances today. In the mid-2000s AAA rated mortgage-backed securities were ‘worth’ 100 cents / dollar until they weren’t. Modern bankers aren’t paid to imagine a different future.

Record profits suggest that companies don’t need cheap loans to invest in productive capacity— they can use their record profits to do so. But the facts are that corporate executives are using corporate profits and cheap loans to buy back company shares. In other words, the ‘zero lower bound’ has no bearing on the decision to invest in productive capacity. The coincidence of cheap money and record corporate profits creates a paradox— the argument that companies can’t invest because they lack the funds to do so, the raison d’etre of the zero lower bound argument, makes no sense when companies have all the money they could ever need from profits and still choose not to invest. Record profits indicate that companies (actually, a few executives) are being very well paid not to invest in productive capacity.

For a practical example, oil and gas drilling bonds will serve the purpose (see this presentation by Art Berman posted by Yves Smith on nakedcapitalism.org). The ‘official’ yield on a two year treasury bond is 0.59%. Investing in an oil and gas drilling company that is losing money (spending a dollar to earn 90 cents) might look like this: Bond bought at par yields 10%, collateral value in workout of 90%, bond is held for three years, two where interest is paid and one year in workout. The annualized yield over three years is 3.7% (formula: ((1.1^2)-1.1)/3) for investing in a money losing business versus 0.59% for investing in a two year treasury note. There is more risk with the drilling bond, but that is the point. It makes no economic sense to spend one dollar to earn 90 cents by investing in the company directly. But in a world flooded with Central Bank money, there are plenty of financial games to be played that make (some) economic sense.

The choice of oil and gas drilling bonds (above) was not coincidental. Monetary policy relates directly to U.S. oil imperialism by what types of companies Wall Street funds. Lenders prefer to make loans against tangible collateral. A promising business plan is not tangible collateral but a uranium mine, real estate and oil and gas resources are. Fracking in the U.S. and tar sands oil extraction in Canada are extremely inefficient sources for oil and gas because the cost per unit of oil or gas recovered is very high (link above) and the environmental costs are several multiples of the value recovered. ‘Loose’ monetary policies tend to drive money to the least economically productive and the most environmentally destructive sectors because these are the most conducive to late-cycle high yielding (until they default) Ponzi finance schemes. In the housing boom financiers made mortgage loans they knew would never be repaid. Likewise extractive industries play collateral games in the face of declining cash-flows until their sector implodes.

One more point on this topic: with corporate profits at record highs corporations could be paying their workers a lot more but they are choosing not to. The point: within the national and mainstream economic frames ‘we are all in this economy together.’ Corporate executives are making it abundantly clear that their view is that ‘their’ interests as corporate managers and as self-endowed ‘owners’ are diametrically opposed to the interests of labor. While this news is a century or two late for those of Marxian inclination, it is likely a revelation for the kids who signed up to fight for Exxon Mobil in Iraq and the American middle class that sees itself one day getting rich by working hard. The bad news: there exists a class whose wealth depends on a benevolent Federal Reserve and keeping everyone else poor. In what way are we in this together?

Endgame

From the end of WWII through the early 1970s the U.S. used its political, economic, military and monetary hegemony to craft institutions that by and large still nominally exist. As was spectacularly demonstrated by the (George W) Bush administration in Iraq, what has changed is that the rest of the world has recovered its capacity to resist U.S. ambitions. This isn’t to suggest that the U.S. military can’t still kill a lot of people. But the question of why anyone would want to is fundamental to tying down the particular institutional logic that has consumed Western officialdom in recent decades? From Ferguson to Detroit to Greece to Spain to Germany (Blocuppy!) hegemonic ambitions are being met with resistance.

In related environs the world of Chauncey Gardiner money managers and free money and lifetime wealth guarantees for corporate executives and financiers continues as standard public policy supported by lobbyists, policy makers, economists and those on the inside. This might be of sociological interest, like cargo cults in Borneo, to the other 99.99% of humanity if it didn’t have direct impact on our lives. As this is being written it appears that much of the rest of the world is running as fast as it can away from U.S. (and Troika) policies. USD hegemony appears to be in the latter stages of the dissolution process begun in the 1970s. As Art Berman’s presentation (link above) suggests, the U.S. has a few years of extremely expensive and environmentally damaging to extract oil and gas supplies before imports are once again essential to continued economic production.

Apparently seeing the writing on the Wall, U.S. President Barack Obama is willing to risk nuclear war with Russia to supply Europe with oil and gas from Iraq and Iran at the cost of countless (infinite) human lives and maintenance of an increasingly costly and ineffectual (except for killing) U.S. military. Fascist wannabes in the NSA, pentagon, FBI and local police forces have turned surveillance, disinformation and political repression into for-profit businesses. Western Central Banks have painted themselves into the proverbial corner by making financial leverage so cheap that a microscopic rise in interest rates will crash world markets. What could have been resolved in 2009, the outsized role of finance and banking in world affairs, has been resurrected like Frankenstein’s monster to contemplate its existence in a world that is better off without it.

The dominant frame of national interests is a central hindrance to social resolution. If Apple Computer and General Electric don’t pay taxes like you and I, what ties our lot to theirs? Liberal economists can argue that the Federal Reserve acts in our interests, but the ‘our’ always put forward is an aggregate. If Charles Koch walks into a bar, everyone in the bar is on average a millionaire. And when he walks back out, they aren’t. Of what relevance then are these aggregates? Most of our lots are more closely tied to those of pensioners in Greece, dispossessed ‘homeowners’ in Spain, the peoples of Russia and Europe being threatened by NATO expansion, the 16,000 ‘criminals’ out of 24,000 citizens in Ferguson, Missouri and the thrown-away kids hopping trains and sleeping under bridges across the U.S.

An economist I respect was asked why officialdom was paying no attention to ideas that would resolve large and growing social problems like poverty, unemployment and homelessness. Despite knowing the economics inside and out, no answer was forthcoming. Left unsaid is that this official disinterest is posed against the most aggressive and sustained efforts in modern history to ‘save’ the bankers and corporate executives that sank the global economy in the mid-2000s. The answer to this indifference is Marx 101— the state exists to support ruling class interests until there is no more ruling class. This is no doubt crude next to endless discussion what the Federal Reserve is really saying. But if we had to attach the facts of the last four decades to a theory that fits, this seems to be the one.

Finally, all economics requires a full accounting of costs for relevance. Wall Street tends to fund the very worst of the extractive industries because they have tangible assets that can be taken if loans aren’t repaid. Because of this banker’s focus on tangible assets, Federal Reserve policies designed to expand bank lending skew ‘the economy’ toward the least productive and most environmentally and socially damaging types of investment. The alternative is fiscal policies that are directed toward full employment and environmental resolution. But the time for constructive policy discussions was 2008 (actually, 1968). This is an argument to end the system that precludes political, social and environmental resolution. Life is for the living. Viva la revolucion!

Rob Urie is an artist and political economist. He fervently hopes to see movement toward social resolution in his lifetime. His book Zen Economics will be made available one way or another in the near future.

Source: http://www.counterpunch.org/2015/03/20/oil-imperialism-and-monetary-policy/

|

|

| |

| Article Rating | Average Score: 0

Votes: 0

| |

|

|